Islamic Society & Culture

Abolition of Slavery:

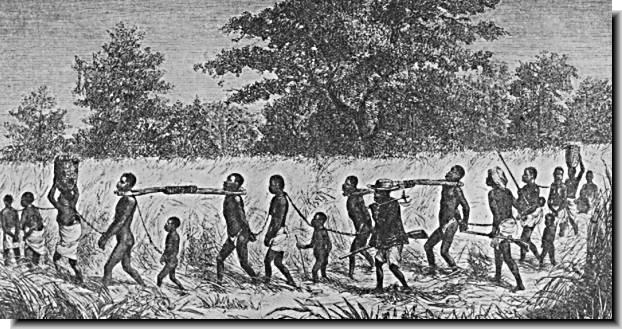

Slavery - International

System: When

the message of Islam was preached, slavery was a very common practice in

all-human societies, it was an international system. The Greeks, Romans, the

ancient Germans whose legal and social institutions have mostly influenced the

modern world, recognized and practiced all kinds of slavery, praedial servitude

as well as household slavery. Slaves were generated in many ways, probably the

most frequent and common was their capture in war, either by design, as a form

of incentive to warriors, or as an accidental by-product, as a way of disposing

of enemy troops or civilians. Other methods of slavery was kidnapping through

slave-raiding or piracy expeditions. Many slaves were the offspring of slaves.

Some people were enslaved as a punishment for crime or debt; others were sold

into slavery by their parents, other relatives, or even spouses, sometimes to

satisfy debts, sometimes to escape starvation. A variant on the selling of

children was the exposure, either real or fictitious, of unwanted children, who

were then rescued by others and made slaves. Another source of slavery was

self-sale, undertaken sometimes to obtain an elite position, sometimes to

escape destitution. Although slavery existed almost everywhere, it seems to

have been especially important in the development of two of the world's major

civilizations, Western (including ancient Greece Rome

Slavery

among Hebrews and Christianity:

Slavery as it existed under

the Mosaic Law has no modern parallel. That law did not originate but only

regulated the already existing custom of slavery: “As for your male and female

slaves whom you may have: you may buy male and female slaves from among the

nations that are round about you. You may also buy from among the strangers who

sojourn with you and their families that are with you, who have been born in

your land; and they may be your property. You may bequeath them to your sons

after you, to inherit as a possession for ever; you may make slaves of them,

but over your brethren the people of Israel 21:20 -21,26-27; Joshua;9:6-27). The gospel in its spirit and

genius is hostile to slavery in every form, which under its influence is

gradually disappearing from among men. The Hebrews practiced two forms of

slavery, the Israelites and non Israelite slaves. The Israelites were enslaved

in bondage as a punishment of a crime or to clear debt, legally they could gain

freedom after six years of servitude. The non Israelites captured in wars or

purchased were not entitled to gain freedom and were maltreated. Christianity

as a religion did not oppose slavery. Except general advice to the masters to

give due to the servants, the teachings of Jesus did not express disapproval of

slavery. Christianity did nothing to eliminate slavery, even the Church held

slaves and considered it to be a lawful system. The cruel treatment of locals

& slaves in America is well known.

Gradual

Elimination of Slavery by Islam:

Islam does not approve of slavery. Islamic legislation

includes a variety of ways to ensure the reduction and eventual eradication of

slavery. As the atonement for many offenses, granting freedom to a slave in

addition to repentance was made obligatory. A portion of Zakah funds

(Charitable donations) was also used to help anyone who could buy his own

freedom in return for a sum of money, which he would pay to his master.

Alternatively, slaves would be bought with Zakah funds and then set free by the

Muslim authorities. According to Qur’an:

“- - - Alms- - -For the freeing of people in bondage - - -This is a duty

ordained by Allah, and Allah is All-knowing, Wise.”(Qur’an;9:60). The

institution of slavery was discouraged and the owners and other people were

enjoined to give financial help to the slaves to earn their freedom under the

law of Mukatabat and marriage with virtuous slaves. Allah says in Qur’an:

“..And if any of your slaves ask for a deed in writing (to enable them to earn

their freedom for a certain sum) give them such a deed if ye know any good in

them; yea give them something yourselves out of the means which Allah has given

to you…”(Qur’an;24:33). “Marry those among you who are single or the virtuous

ones among your slaves male or female..”(Qur’an;24:32).

Narrated by Abdullah

ibn Umar; The

Prophet (peace be upon him) said: “There are three types of people whose prayer

is not accepted by Allah: One who goes in front of people when they do not like

him; a man who comes dibaran, which means that he comes to it too late; and a

man who takes into slavery an emancipated male or female slave.”(Sunan of

Abu-Dawood Hadith 593). "A man came to the Prophet (peace be upon him)

and said to him: 'Guide me to a deed that makes me close to Heaven and far from

Hell.' The Prophet (peace be upon him) said: 'Free a person and redeem a

slave.' " (Fiqh-us-Sunnah Fiqh 3.67). Narrated by Abu

Huraira; The

Prophet (peace be upon him) said, "Whoever frees a Muslim slave, Allah

will save all the parts of his body from the (Hell) Fire as he has freed the

body-parts of the slave." Said bin Marjana said that he narrated that

Hadith to 'Ali bin Al-Husain and he freed his slave for whom 'Abdullah bin

Ja'far had offered him ten thousand Dirhams or one-thousand Dinars.(Sahih

Al-Bukhari Hadith, 3.693). Narrated by Al Marur bin Suwaid; I saw Abu Dhar Al-Ghifari

wearing a cloak, and his slave, too, was wearing a cloak. We asked him about

that (i.e. how both were wearing similar cloaks). He replied, "Once I

abused a man and he complained of me to the Prophet (peace be upon him). The

Prophet (peace be upon him) asked me, 'Did you abuse him by slighting his

mother?' He added, 'Your slaves are your brethren upon whom Allah has given you

authority. So, if one has one's brethren under one's control, one should feed

them with the like of what one eats and clothe them with the like of what one

wears. You should not overburden them with what they cannot bear, and if you do

so, help them (in their hard job)."(Sahih Al-Bukhari Hadith, 3.721).

Like the nuisance of Riba (Usury), in the present

time, the evil of slavery was so much ingrained in the society that its

elimination had to come gradually as Muslim society developed. There was an

important reason for that, which is to help slaves cope with their new status.

Had Islam issued an order to free all slaves straightaway, that would have created

social chaos, as many would not have been able to cope. This happened in the US

Views of Non Muslims Scholar:

The renowned Orientalist Annemarie Schimmel in the book titled "Islam: An Introduction” has comprehensively summarized the Slavery in Islam; “Slavery was not abolished by the Koran, but believers are constantly admonished to treat their slaves well. In case of illness a slave has to be looked after and well cared for. To free (manumit) a slave is highly meritorious; the slave can ransom himself by paying some of the money he has earned while conducting his own business. Only children of slaves or non-Muslim prisoners of war can become slaves, never a freeborn Muslim; therefore slavery is theoretically doomed to disappear with the expansion of Islam. The entire history of Islam proves that slaves could occupy any office, and many former military slaves, usually recruited from among the Central Asian Turks, became military leaders and often even rulers as in eastern Iran, India (the Slave Dynasty of Delhi), and medieval Egypt (the Mamluks).”

The renowned Orientalist Annemarie Schimmel in the book titled "Islam: An Introduction” has comprehensively summarized the Slavery in Islam; “Slavery was not abolished by the Koran, but believers are constantly admonished to treat their slaves well. In case of illness a slave has to be looked after and well cared for. To free (manumit) a slave is highly meritorious; the slave can ransom himself by paying some of the money he has earned while conducting his own business. Only children of slaves or non-Muslim prisoners of war can become slaves, never a freeborn Muslim; therefore slavery is theoretically doomed to disappear with the expansion of Islam. The entire history of Islam proves that slaves could occupy any office, and many former military slaves, usually recruited from among the Central Asian Turks, became military leaders and often even rulers as in eastern Iran, India (the Slave Dynasty of Delhi), and medieval Egypt (the Mamluks).”

Prohibition of Riba (Usury):

History

of Usury in Judaism & Christianity:

In modern law usury, is the practice of

charging an illegal rate of interest for the loan of money. In

Old English law, the taking of any compensation whatsoever was termed usury. With the expansion of

trade in the 13th century, however, the demand for credit increased,

necessitating a modification in the definition of the term. Except for

Genesis; 23:9, Jeremiah;32:10, and Ruth; 4:8, Scripture makes no reference to

transaction procedures. Interest is however prohibited in Bible: “Take no

interest from him or increase, but fear your God; that your brother may live

beside you. You shall not lend him your money at interest, nor give him your

food for profit.”(Leviticus;25:39-37

also Deuteronomy; 23:19 -20).

The violation of this law was viewed as a great crime (Psalms;15:5; Peter;

28:8; Jeremiah; 15:10 ).

After the Return, and later, this law was much neglected (Nehemiah; 5:7,10).

The Jews consider that usury is prohibited with in Jews and that they could

charge interest from gentiles: “Unto a

stranger thou mayest lend upon usury; but unto thy brother thou shalt not lend

upon usury: that the LORD thy God may bless thee in all that thou settest thine

hand to in the land whither thou goest to possess it.”(Deuteronomy;23:20 ). Thus the Jews became to be

known as money lenders, hated by the masses in Europe

due to their exploitation by Jews who charged the interest at exorbitant rates.

In the Middle Ages the Christian Church attempted to enforce certain moral

commands adverse to commercial transactions. The taking of interest for loans

of money was considered income without true work and, therefore, sinful and

prohibited. There was also an attempt to generalize the idea of a just price.

Although both rules, and especially the former, influenced the law and the

economy for centuries, neither of them finally prevailed in the secular world.

The growth of finances, industry, and land estate ruled the rabbis to develop

laws concerning contracts, partnerships, and legal arrangements to circumvent

the biblical prohibition against usury. A series of modes of

transaction effecting the transfer and acquisition of property evolved. Usury

then was

applied to exorbitant or unconscionable interest rates. In 1545 England United States

Prohibition

of Riba in Islam:

Defining Usury (Riba): Riba (literally ‘usury’ or

‘interest’) is prohibited in Islam, for the principle is that any profit sought

should be through own exertions and at our own expense, not through exploiting

other people or at their expense. The Arabic term Riba is considered synonymous

to ‘usury’ which has been defined in the writings of a number of very early

Muslim scholars, it may help to understand its broader meanings. In his

commentary on the Qur'an, Imam Al-Razi says: "The usury based on time

delay was the type commonly practiced in pre-Islamic days. A man would lend

another person some money for a specified term stipulating that he would charge

him a specified amount every month while the principal amount remained intact.

When the agreed time arrived, the lender would request repayment. If the

borrower cannot pay, he increases the monthly payment and the time of the

loan." Al-Jassas says: "It is well known that usury in pre-Islamic

days was simply a loan given for an appointed time with a stipulated increase.

That increase compensated for delay. This is prohibited by Allah." Mujahid

says: "In pre-Islamic days, when a man had borrowed money from another, he

would come to him and say: I will pay you so and so if you allow me a longer

period for repayment." Qatadah says: "The usury practiced in

pre-Islamic days took the form of a sale made for a specified term. When

payment is due and the buyer does not have the money to pay the seller, he

agrees to pay him extra in return for a postponement." Imam Ahmad ibn

Hanbal defines usury in the same terms, saying: "If a man had lent money

to another and the time of repayment was due, the lender would say to the

borrower: You either pay me now or increase the amount to be paid. If he does

not settle the debt then and there, one agrees to increase the amount and the

other extends the time for repayment." All these definitions agree on the

nature of usury. It is financial compensation for time delay. This is what is

known as "increase in lieu of time extension." All scholars and all

Muslim schools of thought are unanimous that this type of Riba is strictly

forbidden. However as regards to the other explanations of Riba (Usury) there

is room for difference of opinion. 'Umar bin Al-Khattab, (2nd

rightly guided Caliph) according to Ibn Kathir, felt some difficulty in the

matter, as the Apostle left this world before the details of the question were

settled. Riba (Usury) was one of the three questions on which he wished he had

more light from the Prophet (peace be upon him). Muslim scholars, ancient and

modern, have worked out a great body of literature on Riba, based mainly on

economic conditions as they existed at the rise of Islam.

Increase

in Lieu of Quality:

There is another type of

Riba, which is known as "increase in lieu of quality". This takes the

form of exchanging two quantities of the same kind, such as dates for dates,

wheat for wheat, rice for rice. A person may offer 1.5 kilogram of dates or

wheat or rice, etc. in return for one kilogram of the same type but of higher

quality. There is no doubt that there may be several types of the same produce

and their qualities differ immensely. Prices could range from the very cheap to

the very expensive, with the latter being two or three or four times as much as

the price of the former. It is conceivable that people would like to barter

some of their produce for a smaller amount of a higher quality type. But this

again is forbidden in Islam as evident from Hadith of Prophet Muhammad(peace be

upon him); Narrated by Abu Said al Khudri: Once Bilal brought Barni

(i.e. a kind of dates) to the Prophet and the Prophet asked him, "From

where have you brought these?" Bilal replied, "I had some inferior

type of dates and exchanged two Sa’s (measurement of weight) of it for one Sa

of Barni dates in order to give it to the Prophet (peace be upon him) to eat."

Thereupon the Prophet(peace be upon him)

said, "Beware! Beware! This is definitely Riba! This is definitely

Riba! Don't do so, but if you want to buy (a superior kind of dates) sell the

inferior dates for money and then buy the superior kind of dates with that

money."(Sahih Al-Bukhari Hadith 3.506). Narrated by Ibn

Umar: At an other occasion the Prophet (peace be upon him) said; "The selling of wheat for wheat is

Riba except if it is handed from hand to hand and equal in amount. Similarly

the selling of barley for barley, is Riba except if it is from hand to hand and

equal in amount, and dates for dates is usury except if it is from hand to hand

and equal in amount. (Sahih Al-Bukhari Hadith 3.379).

Modern

Banking Transactions:

While there are some differences

between such usurious practices and banking transaction in today’s world; but

there are also essential similarities. In a loan obtained from a bank, a

borrower pays a regular amount of interest, which does not affect the

principal. This is similar to the practice of pre-Islamic days when a borrower

used to pay every month a certain sum to the lender, while the principal

remained the same. Moreover, in a banking transaction, when the loan is repaid

over a longer period of time, the amount of interest charged is also higher,

although its rate may remain the same.

Strict

Prohibition of Riba in Qur’an:

It should be well understood

that there is no case of prohibition stated in the Qur'an more forcefully than

the prohibition of Riba. Allah warns the believers that they must desist from

practicing usury or they would face a war declared on them by Allah and His

messenger (peace be upon him): “O You who believe! Fear Allah and waive what is

still due to you from usury if you are indeed believers; or war shall be

declared against you by Allah and His Apostle. If you repent, you may retain

your principal, causing no loss to debtor and suffering no

loss.”(Qur’an;2:278-279). However some eminent scholars have argued that

banking transactions and the system of interest is different from Riba as

called in Islam (?)

The Islamic law of

transactions

as a whole is dominated by the doctrine of prohibition of Riba. Basically, this is the

prohibition of usury, but the notion of Riba was rigorously extended to cover,

and therefore preclude, any form of interest on a capital loan or investment.

And since this doctrine was coupled with the general prohibition on gambling

transactions, Islamic law does not, in general, permit any kind of speculative transaction the results of

which, in terms of the material benefits accruing to the parties, cannot be

precisely forecast. The charging of interest is strongly prohibited according

to Qur’an; “Those who devour usury will not stand except as stands one whom the

Evil One by his touch hath driven to madness.

That is because they say: "Trade is like usury but Allah hath

permitted trade and forbidden usury.

Those who after receiving direction from their Lord desist shall be

pardoned for the past; their case is for Allah (to judge); but those who repeat

(the offence) are companions of the fire: they will abide therein (for

ever)”.(Qur’an;2:275). “Allah will deprive usury of all blessing but will give

increase for deeds of charity: for He loveth not creatures ungrateful and

wicked.”(Qur’an;2:276). “That which ye lay out for increase through the

property of (other) people will have no increase with Allah: but that which ye

lay out for charity seeking the Countenance of Allah (will increase): it is

these who will get a recompense multiplied.”(Qur’an;30:39). Prophet

Muhammad (peace by upon him) reemphasized the abolishment of usury in his Last

Sermon at Hajj, he said;” All usury transactions, which have been made in the past

days of ignorance, are hereby abrogated. You may claim only your capital,

neither inflicting nor suffering any injustice. Allah has decreed that no usury

is permissible. The first usury transactions I abrogate are those of my uncle,

Al-Abbas ibn Abdul Muttalib,”. In some Muslim countries efforts are being made

to replace the ‘Interest’ with Islamic compliant substitutes.

Interpretations

of Riba:

Owing to the fact that

interest occupies a central position in modern economic life, and specially

since interest is the very life blood of the existing financial institutions, a

number of Muslims have been inclined to interpret it in a manner which is

radically different from the understanding of Muslim scholars through last

fourteen centuries and is also sharply in conflict with the categorical

statements of the Prophet (peace be on him). According to Islamic teachings any

excess on the capital is Riba (interest). Islam accepts no distinction, in so

far as prohibition is concerned, between reasonable and exorbitant rates of

interest, and thus what came to be regarded as the difference between usury and

interest; nor between returns on bonus for consumption and those for production

purposes and so on. Hence the Islamic

mode of Riba free banking, is gaining popularity. In Islam the basic principles

of the law are laid down in the four root transactions of (1) Sale (bay'), transfer of the ownership or corpus of

property for a consideration; (2) Hire (ijarah), transfer of the usufruct

(right to use) of property for a consideration; (3) Gift (hibah), gratuitous

transfer of the corpus of property, and (4) Loan ('ariyah), gratuitous transfer

of the usufruct of property. These basic principles are then applied to the

various specific transactions of, for example, pledge, deposit, guarantee,

agency, assignment, land tenancy, partnership, and waqf foundations. Waqf is a

peculiarly Islamic institution whereby the founder relinquishes his

ownership of real property, which belongs henceforth to Allah, and

dedicates the income or usufruct of the property in perpetuity to some pious or

charitable purpose.

Inflation:

Inflation is the very real

problem, which makes it difficult for anyone to advance money to another for a

period of time without making a loss on transaction. That not only applies to a

loan given to another person, but also to money kept in a current account,

which pays no interest. Any form of saving which does not give returns, is a

losing value because of inflation. There must be no injustice, perpetrated or

suffered. That is the divine order stated clearly in the Qur'an: “You shall inflict

no injustice and shall suffer none.”(Qur’an;2:279), “O my people! Give full

measure and weight in all fairness. Do not defraud people of their goods and do

not spread mischief in the land.”(Qur’an;11:85). All this requires thorough study so that scholars

are able to come up with answers to present-day problems, instead of applying

the rulings of earlier scholars to later problems. Using interest to offset the

decrease in money value caused by inflation has some merit. Here the purpose is

to maintain the real value of what a person has. The question is whether it is

permissible to do that or not? This is a very difficult question and scholars

have not come up with a definitive ruling on this point. The problem will

remain until a satisfactory answer is found to ensure fairness to investor,

lender and borrower, without exploitation.

Divergent

Opinions:

There are scholars who argue

that fixing a guaranteed rate of returns in advance is acceptable because it

protects the interest of the individual investor. The rector of Al-Azhar has

come strongly in favour of this method. Dr Riazul Hasan Gillani, holds

doctorate from Al-Azhar

University

According to Sheikh Al-Azhar

Dr. Syed Mohammad Tantawi, a prominent modern-day jurist opines that, the government

savings schemes do not fall into the category of Riba at all, because these

are investment schemes and not Qarz schemes. Among the other scholars who think

that the interest is different from usury, most notable is Dr. Ma’roof

Ad-Dawaleebi, who is a scholar of high repute and who has been involved in politics,

being former prime minister in Syria Saudi

Arabia University

of Damascus

Eminent Pakistani scholar,

Javed Ahmad Ghamidi in discussions opines usury to be an evil which is fully

integrated in the present international financial system. It should be replaced

by Islamic financial system at least in the Muslim societies, till then one

should avoid it as far as possible. However, under unavoidable circumstances

one has to live with this evil as was the case of slavery, which was gradually

phased out. He argues that while there is prohibition of taking Riba, there is

no restriction of paying extra on loan because the loan is taken under

necessity or compulsion, according to him, Qur’an and Hadith forbids taking

Riba or assisting in collection of Riba. Taking lead from the Qur’anic doctrine

of necessity, whereby the prohibited (Haram) becomes temporarily permissible

under certain extreme conditions; “…But (even so) if a person is forced by

necessity without willful disobedience nor transgressing due limits thy Lord is

Oft-Forgiving Most Merciful.” (Qur’an;6:145), he opines that the widows,

orphans, sick, retired elders who have no other source of income may invest in

government saving schemes to get subsistence to survive, though Islamic welfare

government should look after them even without investment.

All Types

of Interest, Riba Forbidden:

The majority of Islamic

scholars still consider all types of interest as Riba, hence forbidden. “...There is none who can change His

words..”(Qur’an;18:27 ).

There is no doubt that Riba is prohibited, but there was some thing about Riba

which even 'Umar bin Al-Khattab wanted to know more form Prophet (peace be upon him) before he left

the world. Till Ummah develops a consensus on the serious issue of defining the

Riba, the advice of Prophet Muhammad (peace be upon him) be followed, who

advised the Muslims to consult their hearts after having studied a matter

carefully. Allah knows the matters

of heart well.

Islamic banking provides a good opportunity for the Muslims to avoid Riba.

"Riba is usually translated in Urdu by the word sud, which is of Persian origin and literally means “profit” is antonym being ziyan. Sud is not synonymous with the Quranic term Riba but is synonymous with the Arabic word 'Ribah'. In fact, any attempt to translate the Quranic term, “riba” in any language, is not only futile, but is also the source of much confused thinking on the subject.- [Extract from article by Fazalur Rahman]

The literal meaning of riba (Arabic Quote To Be Added) as illustrated by the Qur’anic usage is:

To grow e.g. (Arabic Quote TBA)

“And thou beholdest the earth barren, then when We send down water upon it, it quickens and grows…” (XXXII: 5)

To increase; to prosper; (Arabic Quote TBA)

“God destroys riba, but makes alms prosper” (II: 276); (Arabic Quote TBA)

“And whatever you invest in riba so that is may increase upon the people’s wealth, it increases not with God;” (XXX: 39);

to rise ( for example of a hill) as, (Arabic Quote TBA)

“ And we gave them refuge upon a height…..” (XXIII: 50);

This is the translation by Mazheruddin Siddiqi of an Urdu article by the author entitled Tahaqiq-I Riba which was published in the monthly Urdu journal of this institute. Fikr-o Nazar i/5 (November 1963). – (Ed.). (Arabic Quote TBA

“As the likeness of a garden upon a hill…” (II:265)

to swell (for example, foam), as (Arabic Quote TBA)

“Then the torrent carried a swelling scum;” (XIII: 17)

to nurture; to raise ( a child); as (Arabic Quote TBA)

“My Lord, have mercy upon them (i.e my parents) as they raised me up when I was little!”(XVII:24) (Arabic Quote TBA)

“Did we not raise thee amongst us as a child?” (XXVI: 18);

augmentation increase in power, etc., as (Arabic Quote TBA)

“He seized them with a surpassing grip…” (LXIX: 10) (Arabic Quote TBA)

“That one Nation be more powerful than another nation.” (XVI : 92)

From the lexical meaning giving above, the technical meaning of the term “riba” is derived, discussed in thearticle in detail

ROLE OF THE INTEREST-RATE IN THE PRESENT-DAY ECONOMY

In the modern science of Economics the rate of interest occupies the same place as price and performs the all-important function that any price-mechanism performs, viz., of regulating the supply and demand of credit and rationing it among the customers. If the rate of interest, i.e., the price of loaning money, is reduced to zero, then we are faced with a limited supply and an infinite demand. It would become impossible to control the rationing of credit available, so to say, and to assign priorities. Especially in a society like ours where there is a great danger of nepotism and corruption, it is well-nigh impossible to conceive that correct priorities and correct amounts will be the order of the day with the optimum use of the available funds for development. At present, however, the rate of interest functions as the objective standard of allocating the credit principle and the real need for a loan is expressed by readiness to pay the proper price, i.e. the interest-rate is arbitrary is absolutely groundless, simply because it is genuinely a price any other price. Mawdudi, explaining the theory which points to the law of supply and demand as the basis of bank-interest, says, “Just think what this comes to mean.” The capitalist does not straightforwardly and by fait means enter into partnership with the businessman, and obtain his rightful share in the profits earned by him (the businessman). On the other hand, he makes a rough estimate of the minimum profit likely to be made by the businessman. Therefore, he says to himself, ‘I should receive so much interest on the money I loan out to him’. The businessman too, on his part, makes a rough estimate of the maximum profit he is likely to earn from the amount of credit he is going to obtain. Therefore, he says to himself, ‘the interest that I pay should not exceed beyond this point’. Thus both the debtor and the creditor indulge in speculation.”

It seems that Mawdudi has not made a serious study of our present banking system. The kind of picture he has in mind of haggling and of mutual adjustment between the needs of the debtor and the creditor may be true of the usurious practices of the baniya, but is not all true of the financial system banks. The prices in petty business may rise or fall, and, in fact they usually do so, but the rate of interest does not rise or fall even by half or one-fourth per cent except under the stress of diverse and multiple economic factors, and such a rise or fall in the rate of interest itself becomes an important economic factor. The fixation and determination of the rate of bank-interest is not the result of any simple mutual understanding between the debtor and the creditor but the outcome of many complex economic factors.

In the opinion of some economist, the rate of interest can be brought down to zero. In fact the general trend of the economic system has been towards the lowering of the rate of interest. But this can come about only if the volume of the real wealth and state of equality or near-equality comes to exist between supply and demand of money and credit becomes very easy. But this has not been achieved yet even by highly developed countries like the United States. To bring about such conditions in our country, we shall have to make untiring efforts for the production of real wealth and for the formation of capital and unless we succeed in attaining this objective, we shall have to put up with the present rates of interest.

Economists of the Communist school of thought hold a different view of the rate of interest. According to their theory, it is labour only and not capital which produces “surplus value,” i.e. the profit. On this theory, there is no basis at all even for the profits of private business not to speak of the profits made by the banks or the banks-interest. However, the present fiscal system, as it is functioning in Soviet Russia, Yugoslavia and other Communist countries, has to accept bank interest as a necessity contrary to its basic economic theory. The Communist explains this anomaly by treating the present condition as a period of transition in which there can be no escape from bank-interest. They argue that when they have attained their highest ideal, that is of establishing the Communist society organized on the principle, “to every man according to his needs and from every man according to his capacity,” the present banking system with its rates of interest will be abolished. Apart from the question whether or not the system envisaged by Communist is practicable, the difficulty is that if we accept the Communist system, we shall have, also, to accept all it’s regimentations and the coercion employed by it, which, we think, would be resisted by the majority of our people.

As we have, however, explained in the preceding sections of this paper, the general Qur’an teaching wants to develop the maximum of co-operative spirit and socio-economic justice, which is called sadaqah by the Qur’an and which must not be confused with the begging and giving of alms. The co-operative spirit envisaged by the Qur’an was well illustrated by the mu’akhat established by the Prophet after his migration to Medina between the Muhajirun of Mecca and the local Ansar. In the Welfare Co-Operative Commonwealth of Islam, based on the true spirit of sadaqah, bank-interest will certainly be eliminated, because in his ideal Commonwealth, there will be competition among men, but only for virtue and mutual help. To strive to achieve this ideal is the noblest jihad of our times. But if we are to carry on this jihad for the setting up of the Islamic Welfare Co-Operative Commonwealth, it is equally necessary that we should not close our eyes to the present realities, howsoever unpalatable they may be. The abolition of interest presupposes the highest degree imaginable of co-operative spirit and, therefore, cannot be implemented today unless the country’s economy and production are to be left in the direst jeopardy. At present this type of Islamic spirit of co=operation is wanting in our society and, indeed, we are now at the opposite pole from the social order envisaged by the Qur’an. This being the case, it will become particularly impossible for the government to raise interest-free loans for it’s basic non-profit-making projects, such as roads, hospitals, schools, etc. No economy can be built today, nor was one built by our forefathers on qard hasan (qardah-yi hasanah), although private institutions should be encouraged in this direction for purely philanthropic purposes. We, therefore, conclude that the abolition of interest in the present state of our economic development would be a cardinal error.

CONCLUSION

1.(a) The clear words of the Qur’an, “Consume not riba with continued redoubling.

(b) The chronological order in which the verses prohibiting riba were revealed.

(c) The historical traditions concerning the nature of riba going back to the eminent tabi’z commentators of the Qur’an.

(d) The hadith-material describing the historical context in which the verse “remit what is left of riba” was revealed,-all this evidence establishes the following definitions of riba:

“Riba is an exorbitant increment whereby the capital sum is doubled several-fold, against a fixed extension of the term of payment of the debt.”

2. The prohibition of this riba by means of law is a religious necessity.

3. The Qur’an has declared that the opposite of riba is sadaqah which is by no means a form of beggary. In view of this it is the moral duty of the Muslims to build up a system of economy based on sadaqah, i.e. co-operation and mutual consideration. Co-operative effort of the Government and the people is needed to achieve this goal.

4. The basic moral idea underlying the Qur’anic prohibition of riba has been given a wider extension and application in the hadith literature, but the contradictions and inconsistencies in the riba-hadith and the evolutionary trend in this literature leading to an ever-increasing rigidity vitiate its authenticity and authority.

5. The passion for sadaqah inculcated by the Qur’an and the way in which the hadith-material supports and elaborates this idea lead to the conclusion that all immoral forms of financial and economic transactions fall under the category of what Ibn Qayyim calls “concealed riba”. But it is necessary to maintain a distinction between the Qur’anic riba, and the term ‘riba’ as used in later times and by later writers.

6. The system of economy which the Qur’an requires us to establish, being based on the spirit of co-operation, the further nourishment and development of this spirit in the right manner and the reconstruction of society in accordance therewith would make bank-interest and the present banking system quite superfluous which is just what the spirit of the Qur’an and the Sunnah requires of us.

7. As long as our society has not been reconstructed on the Islamic pattern outlined above, it would be suicidal for the economic welfare of the society and the financial system of the country and would also be contrary to the spirit and intentions of the Qur’an and Sunnah to abolish bank-interest.

8. In accordance with the principle of (Arabic Quote TBA) or “graduation” and (Arabic Quote TBA) or “the easing of the way”, it would be necessary to enact legislation against such grave social inequities as feudalism and hoarding, etc. before proceeding to abolish bank-interest.

9. It would be necessary for every citizen of Pakistan to work arduously and with an untiring zeal to reach the desirable goal of reducing bank-interest to the zero point, in other words, to eliminate it completely. For this end, it would be necessary to increase the volume of real wealth and credit capital in the country to such a point that an equality or near-equality comes to exist between the supply and demand of money in credit, and credit becomes very easy. In such ideal circumstances the motive for bank-interest, and indeed, the profiteering motive may become extinct.

10. The Measures adopted by the Government and the collective efforts made by the Muslims in general, alone will bring into existence that Welfare Co-operative Commonwealth which is the only way to establish the economic system of Islam in the present modern conditions.

Extract from article By Fazulr Rahman (modern scholar) : http://ebooks.rahnuma.org/religion/

http://en.m.wikipedia.org/wiki/Islamic_banking

Islamic banking provides a good opportunity for the Muslims to avoid Riba.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

An Other View on Riba

by Dr.Fazal ur Rehman

"Riba is usually translated in Urdu by the word sud, which is of Persian origin and literally means “profit” is antonym being ziyan. Sud is not synonymous with the Quranic term Riba but is synonymous with the Arabic word 'Ribah'. In fact, any attempt to translate the Quranic term, “riba” in any language, is not only futile, but is also the source of much confused thinking on the subject.- [Extract from article by Fazalur Rahman]

The literal meaning of riba (Arabic Quote To Be Added) as illustrated by the Qur’anic usage is:

To grow e.g. (Arabic Quote TBA)

“And thou beholdest the earth barren, then when We send down water upon it, it quickens and grows…” (XXXII: 5)

To increase; to prosper; (Arabic Quote TBA)

“God destroys riba, but makes alms prosper” (II: 276); (Arabic Quote TBA)

“And whatever you invest in riba so that is may increase upon the people’s wealth, it increases not with God;” (XXX: 39);

to rise ( for example of a hill) as, (Arabic Quote TBA)

“ And we gave them refuge upon a height…..” (XXIII: 50);

This is the translation by Mazheruddin Siddiqi of an Urdu article by the author entitled Tahaqiq-I Riba which was published in the monthly Urdu journal of this institute. Fikr-o Nazar i/5 (November 1963). – (Ed.). (Arabic Quote TBA

“As the likeness of a garden upon a hill…” (II:265)

to swell (for example, foam), as (Arabic Quote TBA)

“Then the torrent carried a swelling scum;” (XIII: 17)

to nurture; to raise ( a child); as (Arabic Quote TBA)

“My Lord, have mercy upon them (i.e my parents) as they raised me up when I was little!”(XVII:24) (Arabic Quote TBA)

“Did we not raise thee amongst us as a child?” (XXVI: 18);

augmentation increase in power, etc., as (Arabic Quote TBA)

“He seized them with a surpassing grip…” (LXIX: 10) (Arabic Quote TBA)

“That one Nation be more powerful than another nation.” (XVI : 92)

From the lexical meaning giving above, the technical meaning of the term “riba” is derived, discussed in thearticle in detail

In the modern science of Economics the rate of interest occupies the same place as price and performs the all-important function that any price-mechanism performs, viz., of regulating the supply and demand of credit and rationing it among the customers. If the rate of interest, i.e., the price of loaning money, is reduced to zero, then we are faced with a limited supply and an infinite demand. It would become impossible to control the rationing of credit available, so to say, and to assign priorities. Especially in a society like ours where there is a great danger of nepotism and corruption, it is well-nigh impossible to conceive that correct priorities and correct amounts will be the order of the day with the optimum use of the available funds for development. At present, however, the rate of interest functions as the objective standard of allocating the credit principle and the real need for a loan is expressed by readiness to pay the proper price, i.e. the interest-rate is arbitrary is absolutely groundless, simply because it is genuinely a price any other price. Mawdudi, explaining the theory which points to the law of supply and demand as the basis of bank-interest, says, “Just think what this comes to mean.” The capitalist does not straightforwardly and by fait means enter into partnership with the businessman, and obtain his rightful share in the profits earned by him (the businessman). On the other hand, he makes a rough estimate of the minimum profit likely to be made by the businessman. Therefore, he says to himself, ‘I should receive so much interest on the money I loan out to him’. The businessman too, on his part, makes a rough estimate of the maximum profit he is likely to earn from the amount of credit he is going to obtain. Therefore, he says to himself, ‘the interest that I pay should not exceed beyond this point’. Thus both the debtor and the creditor indulge in speculation.”

It seems that Mawdudi has not made a serious study of our present banking system. The kind of picture he has in mind of haggling and of mutual adjustment between the needs of the debtor and the creditor may be true of the usurious practices of the baniya, but is not all true of the financial system banks. The prices in petty business may rise or fall, and, in fact they usually do so, but the rate of interest does not rise or fall even by half or one-fourth per cent except under the stress of diverse and multiple economic factors, and such a rise or fall in the rate of interest itself becomes an important economic factor. The fixation and determination of the rate of bank-interest is not the result of any simple mutual understanding between the debtor and the creditor but the outcome of many complex economic factors.

In the opinion of some economist, the rate of interest can be brought down to zero. In fact the general trend of the economic system has been towards the lowering of the rate of interest. But this can come about only if the volume of the real wealth and state of equality or near-equality comes to exist between supply and demand of money and credit becomes very easy. But this has not been achieved yet even by highly developed countries like the United States. To bring about such conditions in our country, we shall have to make untiring efforts for the production of real wealth and for the formation of capital and unless we succeed in attaining this objective, we shall have to put up with the present rates of interest.

Economists of the Communist school of thought hold a different view of the rate of interest. According to their theory, it is labour only and not capital which produces “surplus value,” i.e. the profit. On this theory, there is no basis at all even for the profits of private business not to speak of the profits made by the banks or the banks-interest. However, the present fiscal system, as it is functioning in Soviet Russia, Yugoslavia and other Communist countries, has to accept bank interest as a necessity contrary to its basic economic theory. The Communist explains this anomaly by treating the present condition as a period of transition in which there can be no escape from bank-interest. They argue that when they have attained their highest ideal, that is of establishing the Communist society organized on the principle, “to every man according to his needs and from every man according to his capacity,” the present banking system with its rates of interest will be abolished. Apart from the question whether or not the system envisaged by Communist is practicable, the difficulty is that if we accept the Communist system, we shall have, also, to accept all it’s regimentations and the coercion employed by it, which, we think, would be resisted by the majority of our people.

As we have, however, explained in the preceding sections of this paper, the general Qur’an teaching wants to develop the maximum of co-operative spirit and socio-economic justice, which is called sadaqah by the Qur’an and which must not be confused with the begging and giving of alms. The co-operative spirit envisaged by the Qur’an was well illustrated by the mu’akhat established by the Prophet after his migration to Medina between the Muhajirun of Mecca and the local Ansar. In the Welfare Co-Operative Commonwealth of Islam, based on the true spirit of sadaqah, bank-interest will certainly be eliminated, because in his ideal Commonwealth, there will be competition among men, but only for virtue and mutual help. To strive to achieve this ideal is the noblest jihad of our times. But if we are to carry on this jihad for the setting up of the Islamic Welfare Co-Operative Commonwealth, it is equally necessary that we should not close our eyes to the present realities, howsoever unpalatable they may be. The abolition of interest presupposes the highest degree imaginable of co-operative spirit and, therefore, cannot be implemented today unless the country’s economy and production are to be left in the direst jeopardy. At present this type of Islamic spirit of co=operation is wanting in our society and, indeed, we are now at the opposite pole from the social order envisaged by the Qur’an. This being the case, it will become particularly impossible for the government to raise interest-free loans for it’s basic non-profit-making projects, such as roads, hospitals, schools, etc. No economy can be built today, nor was one built by our forefathers on qard hasan (qardah-yi hasanah), although private institutions should be encouraged in this direction for purely philanthropic purposes. We, therefore, conclude that the abolition of interest in the present state of our economic development would be a cardinal error.

CONCLUSION

1.(a) The clear words of the Qur’an, “Consume not riba with continued redoubling.

(b) The chronological order in which the verses prohibiting riba were revealed.

(c) The historical traditions concerning the nature of riba going back to the eminent tabi’z commentators of the Qur’an.

(d) The hadith-material describing the historical context in which the verse “remit what is left of riba” was revealed,-all this evidence establishes the following definitions of riba:

“Riba is an exorbitant increment whereby the capital sum is doubled several-fold, against a fixed extension of the term of payment of the debt.”

2. The prohibition of this riba by means of law is a religious necessity.

3. The Qur’an has declared that the opposite of riba is sadaqah which is by no means a form of beggary. In view of this it is the moral duty of the Muslims to build up a system of economy based on sadaqah, i.e. co-operation and mutual consideration. Co-operative effort of the Government and the people is needed to achieve this goal.

4. The basic moral idea underlying the Qur’anic prohibition of riba has been given a wider extension and application in the hadith literature, but the contradictions and inconsistencies in the riba-hadith and the evolutionary trend in this literature leading to an ever-increasing rigidity vitiate its authenticity and authority.

5. The passion for sadaqah inculcated by the Qur’an and the way in which the hadith-material supports and elaborates this idea lead to the conclusion that all immoral forms of financial and economic transactions fall under the category of what Ibn Qayyim calls “concealed riba”. But it is necessary to maintain a distinction between the Qur’anic riba, and the term ‘riba’ as used in later times and by later writers.

6. The system of economy which the Qur’an requires us to establish, being based on the spirit of co-operation, the further nourishment and development of this spirit in the right manner and the reconstruction of society in accordance therewith would make bank-interest and the present banking system quite superfluous which is just what the spirit of the Qur’an and the Sunnah requires of us.

7. As long as our society has not been reconstructed on the Islamic pattern outlined above, it would be suicidal for the economic welfare of the society and the financial system of the country and would also be contrary to the spirit and intentions of the Qur’an and Sunnah to abolish bank-interest.

8. In accordance with the principle of (Arabic Quote TBA) or “graduation” and (Arabic Quote TBA) or “the easing of the way”, it would be necessary to enact legislation against such grave social inequities as feudalism and hoarding, etc. before proceeding to abolish bank-interest.

9. It would be necessary for every citizen of Pakistan to work arduously and with an untiring zeal to reach the desirable goal of reducing bank-interest to the zero point, in other words, to eliminate it completely. For this end, it would be necessary to increase the volume of real wealth and credit capital in the country to such a point that an equality or near-equality comes to exist between the supply and demand of money in credit, and credit becomes very easy. In such ideal circumstances the motive for bank-interest, and indeed, the profiteering motive may become extinct.

10. The Measures adopted by the Government and the collective efforts made by the Muslims in general, alone will bring into existence that Welfare Co-operative Commonwealth which is the only way to establish the economic system of Islam in the present modern conditions.

Extract from article By Fazulr Rahman (modern scholar) : http://ebooks.rahnuma.org/religion/

Related:

http://en.wikipedia.org/wiki/Usury

http://en.wikipedia.org/wiki/Usury

Usury War on Humanity - YouTube

www.youtube.com/watch?v=FEheU28ea3cNov 28, 2014 - Uploaded by HourMoneyJubileeUsury War on Humanity .... +HourMoneyJubilee I've been thinking of this concept and I totally agree we need ...

Usury War on Humanity - YouTube

www.youtube.com/watch?v=FEheU28ea3cNov 28, 2014 - Uploaded by HourMoneyJubileeUsury War on Humanity .... +HourMoneyJubilee I've been thinking of this concept and I totally agree we need ...

Usury Is Permitted For The Goyim When It Is A Business ...

www.youtube.com/watch?v=uKj3nl8mB7USep 10, 2014 - Uploaded by 108morris108Judaic law and Thatcherism and Reagonomics may be the same thing. The pious Jewish religion would ...

www.youtube.com/watch?v=Q4uiYi1OOvA

Mar 8, 2015 - Uploaded by RaisingKundalini2

David Pidcock with Daryl Bradford Smith on Zionism, Israel, Interest ("The Key to all the problems"), Usury ...

Usury and the Oppression of the Poor - YouTube

www.youtube.com/watch?v=HOd6EgL2lCU

Aug 23, 2014 - Uploaded by Word of Truth Baptist Church

Usury is oppression. Avoid being brought into bondage. Be wise with your finances. Be generous, especially ...

Usury or bank interest Explained - YouTube

www.youtube.com/watch?v=kX_YW2u8y-U

Mar 1, 2014 - Uploaded by Vic Man

A quick video on how interest on money steals the wealth of others. This is why Governments are now made to ...

What Islam say about Interest/Usury/riba/sood- Dr Zakir Naik ...

www.youtube.com/watch?v=o83pj97NKVM

Nov 14, 2010 - Uploaded by Rameeez420517

What Islam say about Interest/Usury/riba/sood- Dr Zakir Naik ... Are we not ina time when interest/riba/usury ...

https://en.wikipedia.org/wiki/Islamic_banking

http://islam4humanite.blogspot.com/2015/04/riba-usury.html

article By Fazulr Rahman (modern scholar) : http://ebooks.rahnuma.org/religion/

INDEX: